504 Program Rate Update for March 2015 |

4.401% – 10 Year Debenture Effective Rate *4.799% – 20 Year Debenture Effective Rate * |

“And now for something completely different . . . “ |

|

This being March, next to April that cruelest of months, the first uptick in the Twenty Year Debenture rate since September of 2014 came to pass with rates moving up 26 basis points to 2.72%. The booming employment numbers delivered late last week, along with the first glimmers of wage growth clearly point to further economic growth. While this certainly means the beginning of interest rate increases by the Fed, in a return to rate curve normalization, it also indicates possible further growth or at least stability in asset values. To an SBA lender, that means business acquisition loans, as owners who survived the recent unpleasantness, having had all the fun to be had and likely garnered more grey hair than they had bargained for, may now consider selling out in at more reasonable valuations. Business acquisition loan structures can run the full gamut of SBA lending, from 7(a) for goodwill to 504 for either real estate or equipment. Thus let us for once discuss the “stepchild” of 504 lending; the Ten Year Debenture.

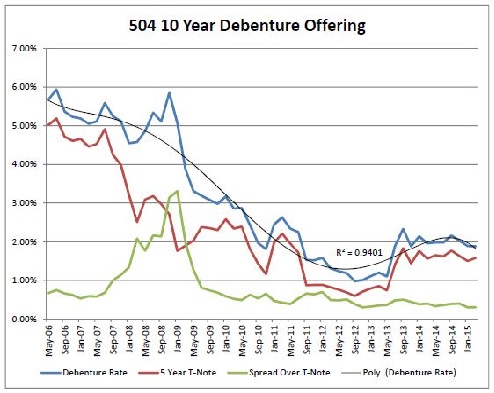

Chart and Statistical Data is from September 2006 to March 2015

The Ten Year Debenture demonstrates a critical difference to the Twenty Year, logically flowing from the shorter term: it more tightly tracks the like term Treasury. (An R2 of 0.94 vs. 0.89 for the Twenty Year) Thus, after the “Taper Tantrum” of May 2013, as short term rates remained elevated in anticipation of imminent action by the Fed, the Ten Year Debenture followed the lead even while longer term rates drifted downward until this month. The 504 Ten Year Debenture offers lenders a way to more effectively segregate risk by placing shorter term assets on appropriate terms. Terms, which are nonetheless more liberal than amortizations available in the market, and at rates superior to market offerings. By using 504 loans as part of a business acquisition, lenders can provide significant fixed rate structures as protection for their borrowers and their institution in a rising rate market. With an almost 40 bps. differential and a much shorter amortization to the Twenty Year Debenture, there is a significant interest savings for a borrower who can handle the cash flow demands. A more detailed discussion, while slightly dated due to regulatory changes, of principles in structuring 504/7(a) business acquisition combination loans is available here (Business Acquisition Financing). One of those regulatory changes is the new availability of the 504 Green capability to make larger loans. We welcome the opportunity to earn your business. * Note: Rates are subject to credit determination & auction pricing. Past performance is no guarantee of future results. Share this message with the tools below. |

{kind=link}